Why dealers hedge (the mechanism)

Understand the feedback loop that connects options dealer positions to spot price.

A dealer doesn't trade options to bet on direction. They sell options to whoever wants to buy them and collect the spread, exactly like a market maker on any other instrument.

The problem: every option they sell creates a directional position they didn't want. To stay neutral, they hedge. That hedging is the entire reason GEX moves price.

The dealer's day

A dealer sells a $100,000 BTC call to a retail trader. From the dealer's point of view, this is a short call position. If BTC rallies, the call gains value — the dealer is on the wrong side.

To neutralize that risk, the dealer buys some spot BTC. Just enough to offset the call's current sensitivity to price. This is delta hedging.

If price never moved, the dealer would set this hedge once and forget it. But price does move, and as it moves, the call's sensitivity to price changes too. The hedge has to be updated. That re-hedging is the loop that moves spot price.

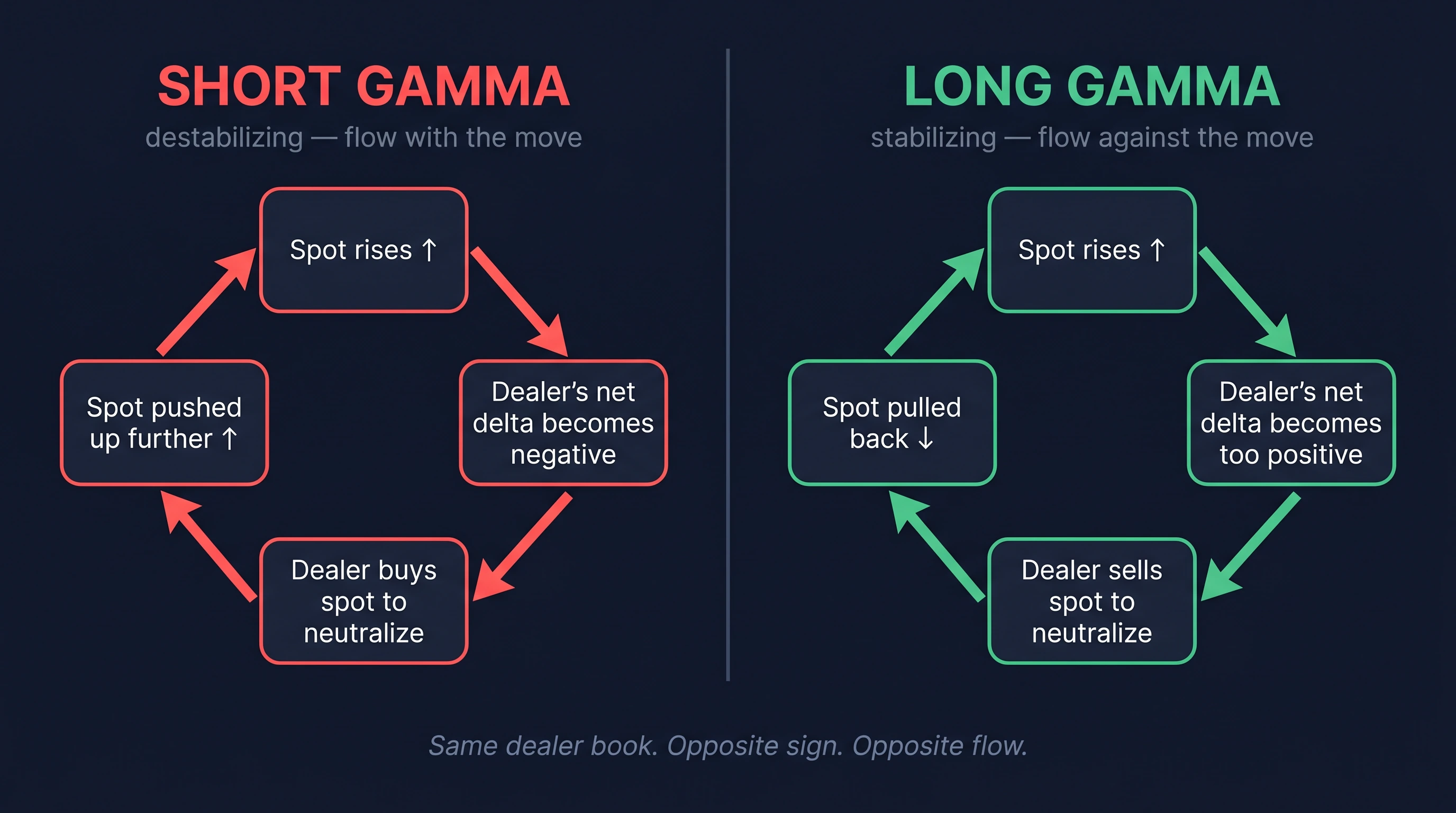

Short gamma: the destabilizing case

When the dealer is net short gamma (which they are most of the time, because retail and institutional flow tends to buy options), their hedge updates work with the market direction.

Walk through it:

- Spot rises by $1,000.

- Their short call's delta gets more negative.

- To stay neutral, they buy more spot.

- Their buying pushes spot up further.

- Repeat.

The same logic in reverse on a fall: more selling into a falling market. Short-gamma hedging is destabilizing — it amplifies whatever direction price is already going.

This is why the negative-gamma regime feels jumpy. Every move triggers more flow in the same direction.

Long gamma: the stabilizing case

Sometimes dealers end up net long gamma — typically after large institutional flow sells options to them in size. The full attribution is a Track 3 topic; what matters here is that when it happens, the loop reverses.

- Spot rises by $1,000.

- The dealer's net delta gets too positive for neutral.

- To rebalance, they sell spot.

- Their selling caps the rally.

On a fall: they buy. Long-gamma hedging is stabilizing — it pushes back against whichever direction price is going.

This is why the positive-gamma regime feels sticky. Every move triggers flow against it.

Why this matters for you

You don't trade options. You don't hedge. But you trade in a market where someone — the dealer — has to hedge regardless of where the market is going.

Their hedging shows up as buying or selling pressure at predictable price levels, in predictable amounts, with predictable behavior. That is what GammaFlip surfaces.

When you see a tall green bar at $98,000, that's a price level where dealer hedging will lean against whatever direction price is moving. When you see a tall red bar at $105,000, that's a level where their hedging will lean with the move.

You are reading their forced flow.

The takeaway

The market has one player who doesn't get to opt out of trading at every price level: the dealer. Their position changes with the market. Their hedging behavior is mechanical. Their flow is observable through GEX.

The next lesson cracks open the math behind "delta changes as price moves" — what gamma actually is, with no formulas.

Dealers hedge because they have to. You're reading the flow they're forced to make.

Check your understanding

Why do dealers hedge in the first place?

Dealers (market makers) sell options to traders without taking a directional view. To stay neutral, they hedge their resulting exposure in the spot market. Without hedging, every option they sell would be a directional bet — and they're not in that business.

What does 'short gamma' mean for a dealer's hedging behavior?

Short gamma means the dealer's delta moves the wrong way as price moves. As price rises, their delta becomes more negative; to stay neutral, they have to buy spot. As price falls, delta becomes more positive; they sell spot. The result: they end up buying highs and selling lows — destabilizing flow that amplifies whatever direction price is going.

Why does a positive-gamma dealer position dampen volatility?

When dealers are net long gamma, the math reverses. They sell into rallies and buy dips to stay neutral — exactly opposite to short-gamma hedging. That dampens moves and creates the 'sticky' regime above the Flip Point.