What gamma actually is

Build an intuitive picture of gamma without formulas: it's how fast an option's price-sensitivity changes.

Two ideas. That's all gamma is.

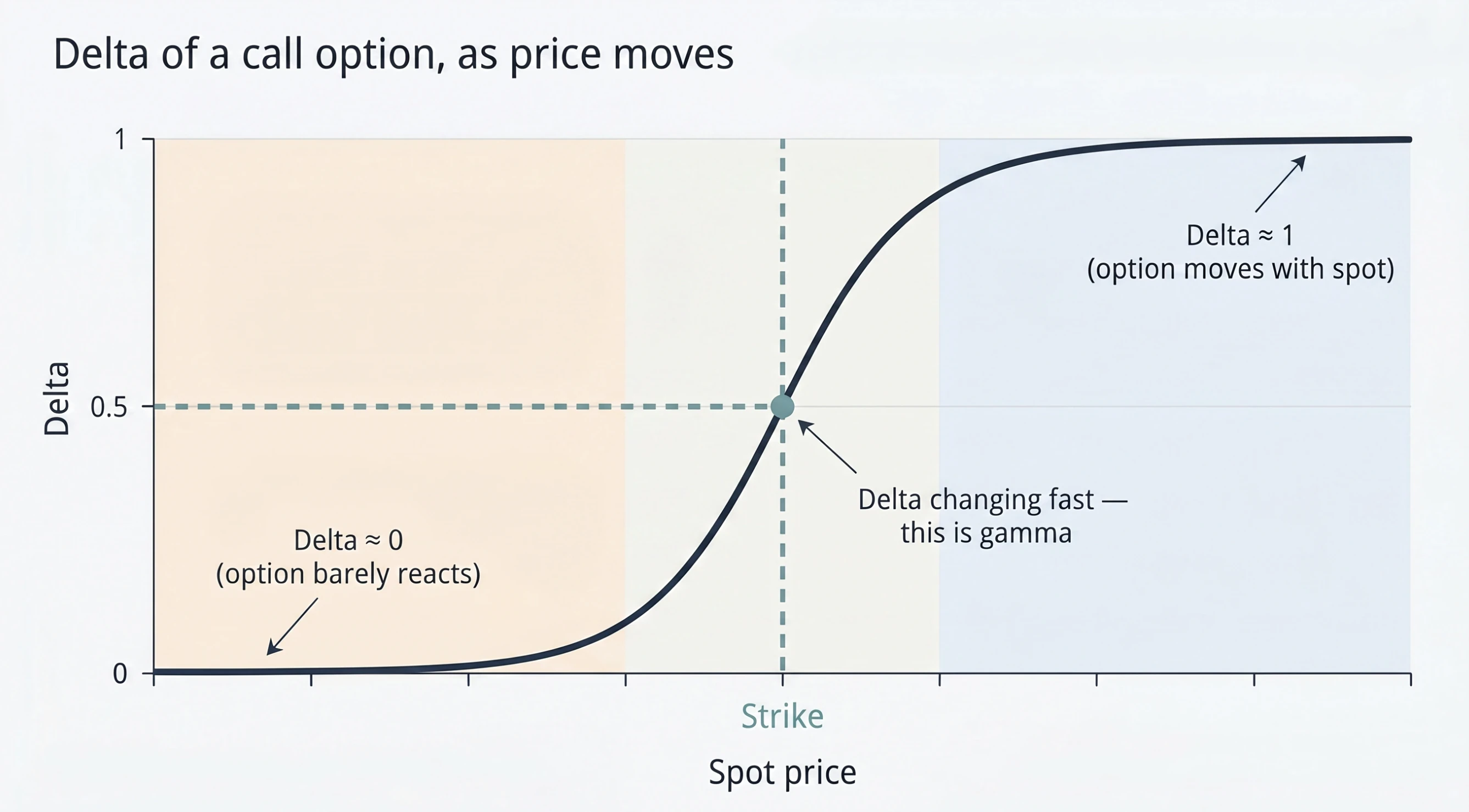

Idea 1 — Delta is a sensitivity dial

When you own a call, how much does its value change if spot moves $1?

That answer is delta. It's a single number between 0 and 1.

- Delta of 0.1 — option barely reacts to price. Either deep out-of-the-money or far from expiry.

- Delta of 0.5 — option moves about half as much as spot. Typically near the strike.

- Delta of 0.9 — option moves almost in lockstep with spot. Deep in-the-money.

For puts, the range is -1 to 0 — same idea, opposite sign.

A dealer hedges by holding the opposite of an option's delta in spot. Sold a call with 0.5 delta? Hold 0.5 of the underlying, long. Now the position is net flat to small price moves.

Idea 2 — Delta isn't fixed

Here's the catch: delta changes as spot moves.

A call that was worthless yesterday becomes meaningful as spot rises toward the strike. Its delta climbs from near 0 toward 0.5 toward 0.9.

That climb has a shape. It's an S-curve.

- Far below the strike — delta is near 0 and barely moves with spot.

- Near the strike — delta accelerates fast. Small spot moves change delta a lot.

- Far above the strike — delta is near 1 and barely moves.

The slope of that curve at any point is gamma.

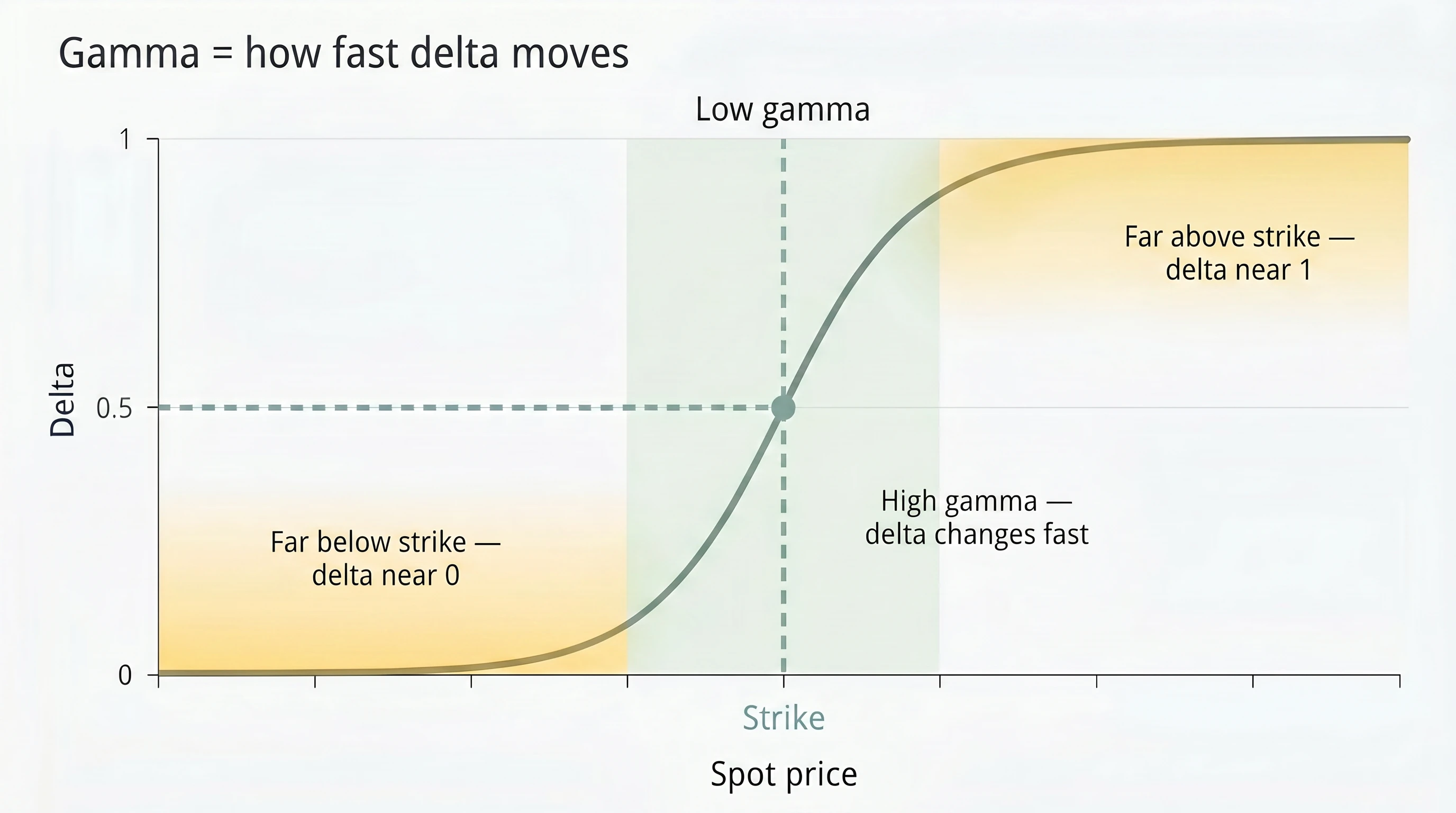

Gamma is curvature

Gamma is how fast delta changes per dollar of spot move.

- Low gamma — delta is stable. Dealer hedges once and is fine.

- High gamma — delta is whipping around. Dealer has to keep re-hedging.

The middle of that S-curve — right around the strike — is where gamma is highest. That's why dealer hedging activity is most intense at strikes price is currently visiting.

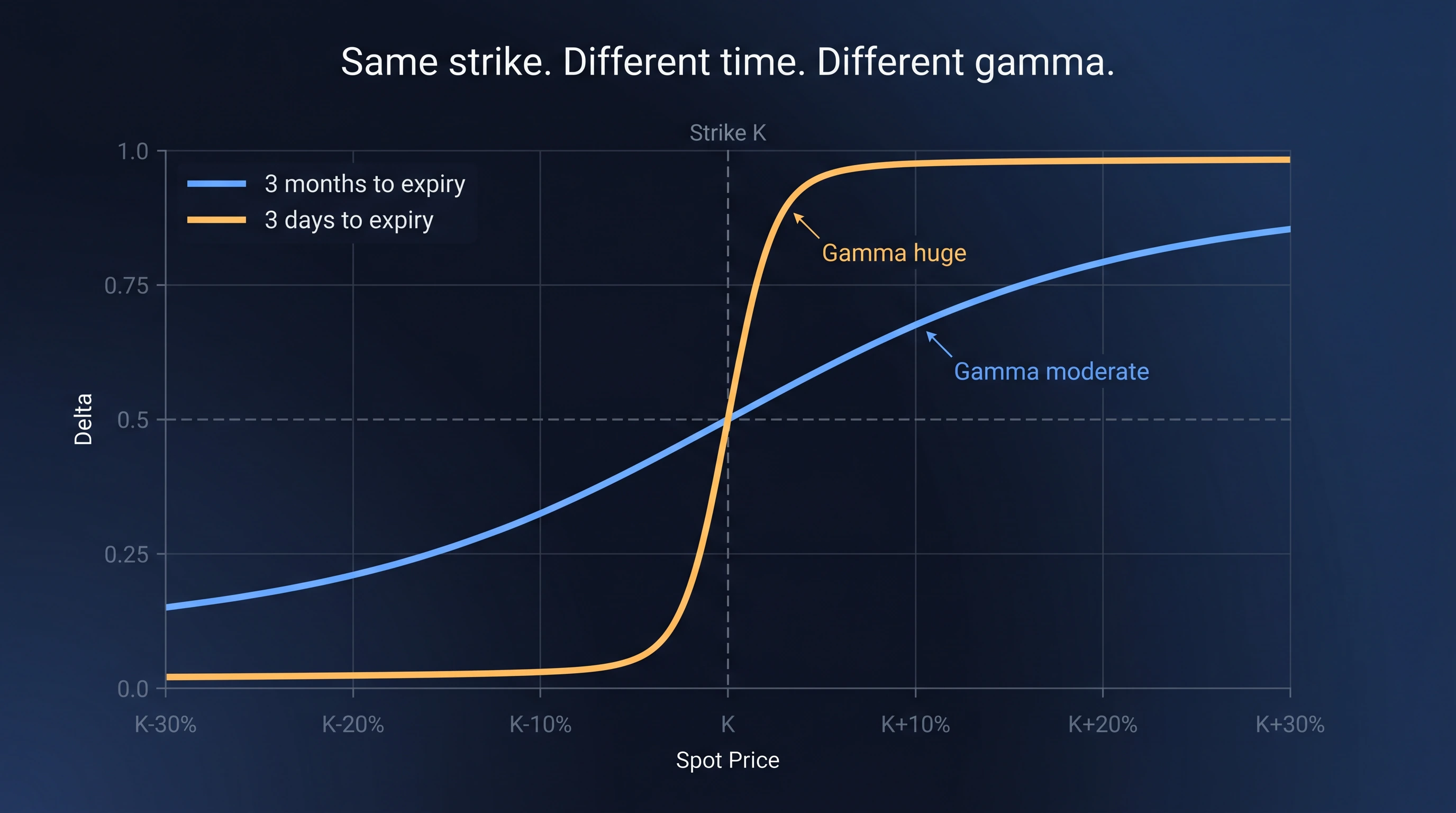

Why time amplifies gamma

The S-curve gets steeper as expiration approaches.

Three months out, an at-the-money call's delta moves slowly — there's still time for almost anything to happen. The slope of the curve is gentle. Gamma is moderate.

Three days out, the same call's delta is binary. Either it expires worthless or it expires in-the-money, and which one depends entirely on whether spot is above or below the strike at the close. The curve becomes nearly a step function. Gamma at the strike is enormous.

This is why the days right before a major expiration produce the most concentrated dealer hedging activity. And why the GEX profile changes so dramatically across a Friday 08:00 UTC settlement.

Why this matters in GEX

GammaFlip aggregates gamma × open interest × dealer position sign across all strikes for the assets and expirations you're looking at. The result is a single bar at each strike showing the net dealer gamma exposure there.

A tall positive bar means: at this strike, dealers are net long gamma. Their hedging will dampen moves through it. Price tends to stick.

A tall negative bar means: dealers are net short gamma. Their hedging will amplify moves through it. Price tends to accelerate.

Now the chart is no longer abstract. It's a map of where dealer hedging behavior changes character.

The takeaway

Delta is sensitivity. Gamma is the rate of change of sensitivity. High gamma = high re-hedging activity. The GEX-by-Strike chart shows you where on the price axis that activity is concentrated.

Next lesson: from gamma at one strike to the GEX bars you actually see in the app.

Delta is sensitivity. Gamma is how fast that sensitivity changes.

Check your understanding

If a call has delta of 0.5, what does that mean?

If spot moves $1, the call is expected to gain about $0.50 — half the move. Delta is the option's price sensitivity to spot. Calls have delta from 0 (worthless out-of-the-money) to 1 (deep in-the-money, behaves like spot itself).

Where is gamma highest for a near-term option?

Right at the strike, especially close to expiration. That's where delta swings most sharply — from 'this option will probably expire worthless' to 'this option is now worth real money' over a small price range. The closer to expiration, the steeper that swing.

Why does high gamma make a dealer's life harder?

High gamma means delta is changing fast as price moves. The dealer's hedge gets stale instantly. They have to trade spot more frequently and in bigger size to keep their position neutral — which is exactly the flow that drives the GEX feedback loop.