Max Pain Explained

Where does Bitcoin "want" to be at expiration?

Every Friday, billions of dollars in crypto options expire. Traders, market makers, and algorithms all jostle around a hidden center of gravity — a price level where the option market inflicts the most pain on the most people.

That level is called Max Pain.

It's one of the oldest options metrics. Every serious options trader has heard of it. But few understand where it fails — and what better alternatives exist.

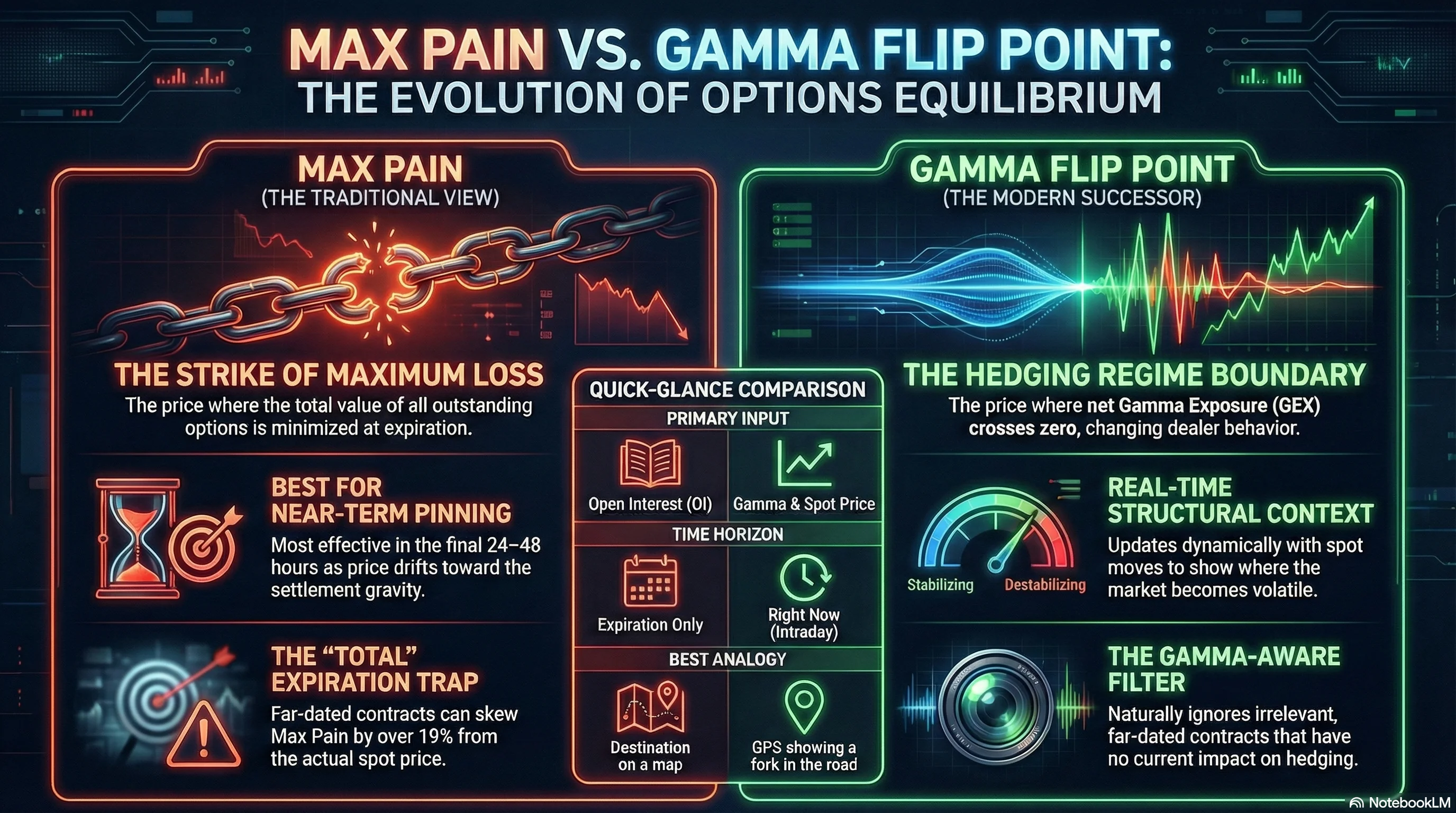

What Is Max Pain?

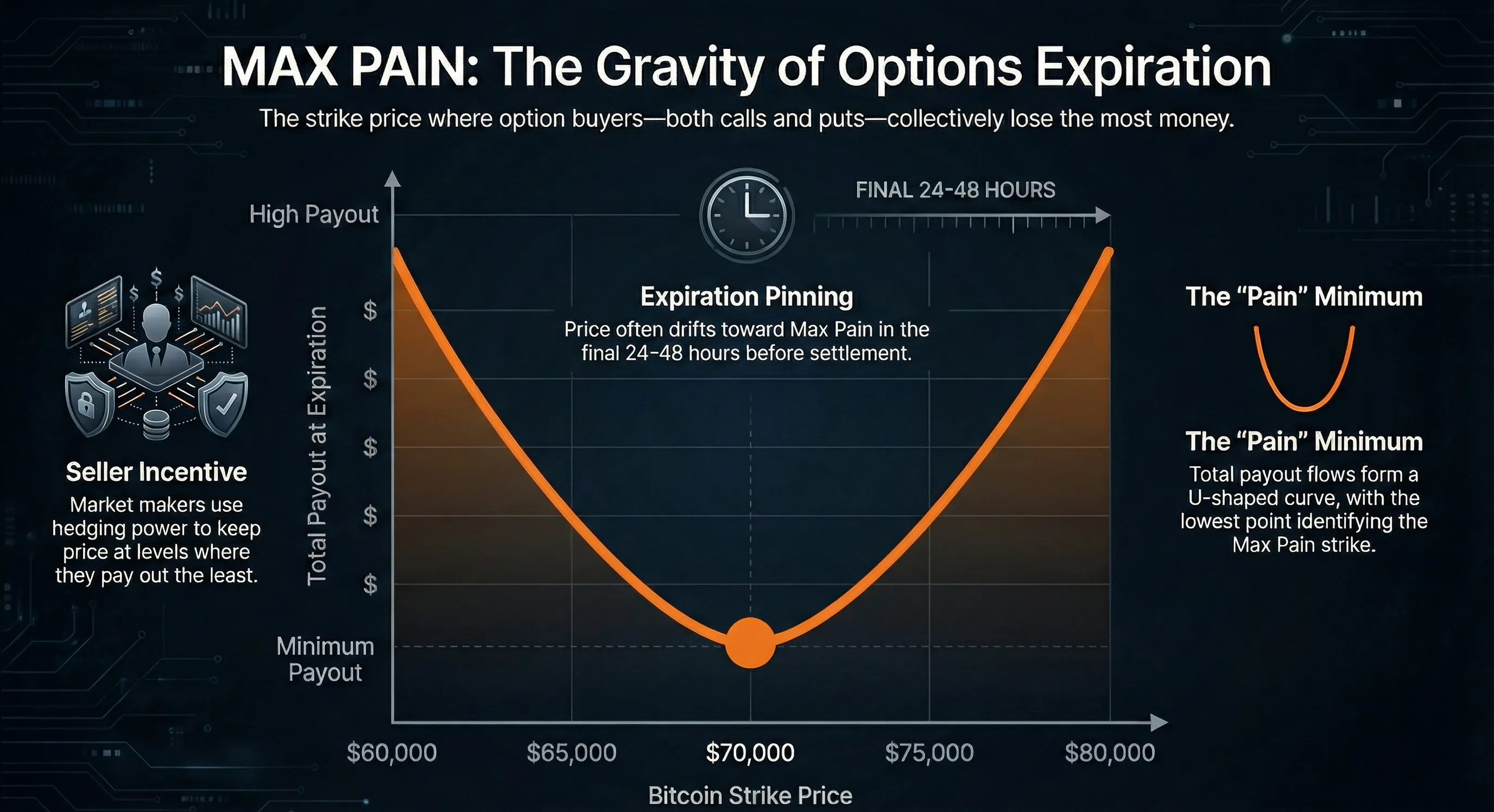

Max Pain is the strike price at which the total value of all outstanding options is minimized at expiration.

In plain language: it's the price where option holders — both call buyers and put buyers — collectively lose the most money.

Option writers (market makers, institutions) have an incentive to keep price at the level where they pay out the least. Since writers collectively have more capital and hedging power than retail buyers, price tends to gravitate toward Max Pain as expiration approaches.

How Is It Calculated?

For each possible settlement price, sum up all in-the-money payouts across every call and put. Max Pain = the price where total payout is smallest.

No Greeks, no volatility surface, no Black-Scholes. Just open interest and intrinsic value.

Where Max Pain Works

- Expiration pinning. In the final 24–48 hours before settlement, delta-hedging flows and OI concentration often cause price to drift toward Max Pain.

- OI sentiment gauge. A large gap between spot and Max Pain reveals directional bias in positioning.

- Simple, universal, objective. No parameters to tune, no model assumptions. Every platform computes it the same way.

Where Max Pain Breaks

It Ignores the Greeks

Max Pain uses raw OI — it doesn't account for gamma, delta, or any measure of how options currently affect dealer hedging. A $150K BTC call with 5,000 OI carries the same weight as a $70K call with 5,000 OI, even though one is deep OTM with near-zero delta and the other is driving real hedging flows.

The "TOTAL" Expiration Trap

This is where Max Pain most commonly misleads. When you combine all expirations into one TOTAL view, far-dated contracts (3–12 months out) with massive OI at round-number strikes ($100K, $120K, $150K) fully count toward Max Pain — even though they have zero impact on today's hedging.

We validated this empirically. On February 10, 2026, with BTC at $68,662:

| Metric | Value | Delta from Spot |

|---|---|---|

| Near-term Max Pain (DTE 0–9) | ~$70,000 | +1.9% |

| TOTAL Max Pain | $82,000 | +19.4% |

Near-term Max Pain was sensible. TOTAL Max Pain was dragged $13K above spot by far-dated open interest.

The Gamma Flip Point: A Modern Alternative

If Max Pain asks "where does OI want price at expiry?", the Gamma Flip Point asks:

At what price do dealers switch from stabilizing the market to destabilizing it?

The Flip Point is the price where net Gamma Exposure (GEX) crosses zero:

- Above the Flip: Dealers are long gamma — they buy dips and sell rallies. Price is dampened.

- Below the Flip: Dealers are short gamma — they sell dips and buy rallies. Price is amplified.

The key difference: gamma is in the formula, which naturally filters out irrelevant contracts. Deep OTM options and far-dated expirations have gamma near zero — they contribute almost nothing, regardless of OI size. Only contracts actively affecting dealer hedging make it through.

Max Pain vs Flip Point: Side by Side

| Max Pain | Flip Point | |

|---|---|---|

| What it measures | OI-weighted expiration equilibrium | Gamma-weighted hedging regime boundary |

| Inputs | Strike × OI × intrinsic value | Strike × OI × gamma × spot² |

| Time horizon | At expiration | Right now |

| Best for | Single near-term expiration | Any timeframe, especially TOTAL |

| Weakness | Ignores Greeks; far-dated OI skew | Requires gamma data (not always available) |

| Updates when | OI changes | OI changes OR spot moves |

| Analogy | Destination on an old map | GPS showing where the road forks |

When to Use Which

Max Pain when you're analyzing a single near-term expiration, watching for expiration pinning in the final 24–48h, or reading OI sentiment bias.

Flip Point when you're trading intraday or multi-day, analyzing TOTAL expiration, or setting entries and stops based on structural levels.

Together: Max Pain for strategic context (where does OI lean?), Flip Point for tactical execution (where does the hedging regime change?).

Key Takeaways

-

Max Pain is the strike where total option payout is minimized at expiration. It works best for single, near-term expirations.

-

TOTAL Max Pain is misleading. Far-dated OI drags it away from spot with no bearing on current dynamics.

-

The Flip Point is the gamma-aware equilibrium. It's dynamic, structurally coherent, and directly maps to the dealer hedging regime — making it more actionable for real-time trading.

Info

Disclaimer: This article is for educational purposes only. Options metrics like Max Pain and the Gamma Flip Point describe market structure — they are not price predictions. Past patterns do not guarantee future results. Always use proper risk management and consider multiple data sources before making trading decisions.

Ready to see GEX in action?

Try GammaFlip.io and experience professional-grade gamma exposure analysis

Launch App